The Fed recently announced they would aim to raise interest rates and reduce their balance sheet. Like clockwork, Goldman Sachs, Moodys, Deutsche Bank and various economists came out and predicted a recession. Personally I do think the chance of a recession within the next two years is pretty high – I’d say it’s about 50%. But in the long run I don’t think it will make much difference.

The Fed’s mandate is to target inflation of 2 percent and an unemployment rate of 4.1 percent. Never mind that ultimately both are fairly arbitrary numbers, and that the formula for calculating either is changing continuously. This is the big, flashing goal they have broadcasted to the world. Additionally they are desperate to get back to “normal” interest rates, which in their mind is a range of 3% ~ 7%, which is something that the US hasn’t experienced consistently for more than 20 years.

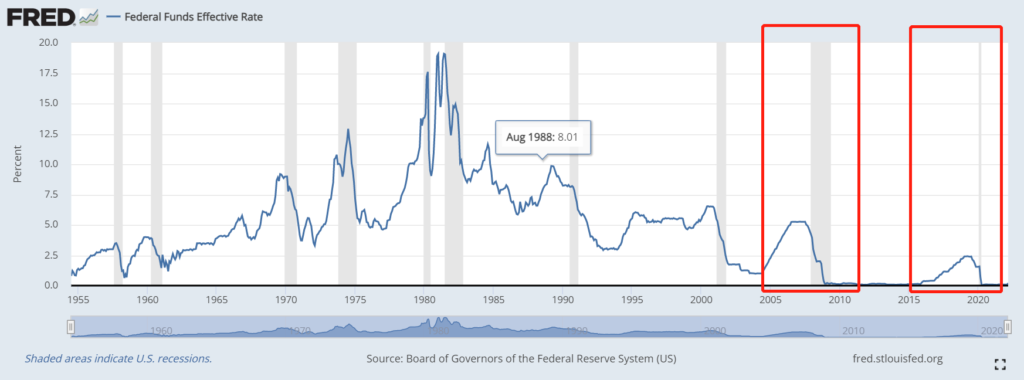

There have been two attempts to get back to “normalcy”, in 2006 and 2019. Guess what happened? Recession.

What they are really trying to do is both preserve their own influence and enact the agenda of the Biden administration. When central banks maintain near-zero rates for a long time, their ability to influence the economy declines. We see this with the ECB and BOJ. In a separate but related fashion, when central banks repeatedly back down in the face of economic pushback, their influence also declines. We see this with the PBOC. Both are happening to the Fed and it’s part of why they’re desperate to get back to “normal” rates.

Additionally, the Biden administration has made it a core plank of their platform to reduce wealth inequality. It is obvious to just about everyone the Fed’s loose monetary policy has increased wealth inequality. It is equally obvious they can’t say this out loud, and must continue to pretend to be bewildered by what has happened while endlessly “conducting research to better understand what contributes to economic inequality in its many forms“. In theory, tightening monetary policy arrests asset growth, lowers inflation, and hardens the currency. In general this benefits economic actors who are paid a wage. Loose monetary policy does the opposite.

The investment banks also have a dual mandate – to their clients and to their staff. For the most part both benefit from loose monetary policy. Their clients benefit because they’re usually rich people, and benefit from asset growth. People who work at banks are mostly “normal” people who earn a wage, however they all do well when the bank does well, and the bank does well when business is good. So it is no surprise Goldman is publicly saying the sky will fall if the Fed raises rates. Furthermore, Wall Street is not really a collection of independent, rational actors. There are two banks that set the tone and pace, namely Goldman and JP Morgan, and everyone else follows and copies whatever they do. There are obviously exceptions but for the most part this is true.

My point is that Goldman’s announcement, and the oddly coordinated chorus around it is not an isolated event. It’s less a prediction the way a meteorologist would forecast the weather, and more a prediction the way a mobster predicts bad things might happen to you if you don’t pay your dues. Ultimately this is just another episode in a long running struggle over who controls the financial system, and by proxy its impact on the economic system.

It’s also boring because of how remote the possibility is the Fed will accomplish their goals. The Fed has been a tool for enacting policy of the executive branch ever since possibly Hank Paulson (although it’s arguable the Bush administration had no coherent economic policy) and definitely since Bernanke. The Fed is so far down this path that it’s almost inconceivable how it can go back. Raising interest rates is the easy part, since there’s a relatively small distance between 0.5% and 3%, and because it has a delayed impact on the economy. The much more difficult part is flattening out the Fed’s balance sheet, which has grown 10x since 2008. Not only is this a tremendous amount of assets, it’s also while net US treasury issuance is ever increasing because the US government’s budget deficit is ever increasing. There’s nearly no chance at all the deficit will be reduced because two thirds of the budget is mandatory spending, most notably Social Security, Medicare and Medicaid, and of the remainder almost half is for defense, which all of a sudden is popular again due to the war in Ukraine. The Fed selling Treasuries while the federal government also increases sales of Treasuries leads to very, very weird things happening in the financial system that absolutely no one, not the banks, not investors, not the federal government and definitely not the Fed want to see happen. Maybe China and Russia.

Now the people who work at the Fed are very smart, and it is extremely unlikely they really believe, in their heart of hearts, that any of this makes sense. It’s simply the role they play in the financial system, namely being myopic and non-political technocratic wonks. They are supposed to go around telling people that, based on their impenetrable models, following their brand of macroeconomics is supposed to lead to a utilitarian dynamic equilibrium that maximizes utility for all people, if only annoying, unforeseeable and “transitory” external events didn’t get in the way. Therefore they have to periodically pretend they’re trying to get back to this equilibrium. They’re just doing their job.

So long story short, I don’t think there’s anything terribly interesting in either what the Fed is doing or what Goldman and its groupies are saying about it. It’s entirely expected of both parties and probably won’t have much impact on the long-term trajectory. Don’t get me wrong, I think it’s going to suck. I just don’t think it’s worth it for anyone aside from professional hedge fund managers to spend much time worrying about it. For most people, long-term adaptation for a spooky and fragile new normal is probably more productive.