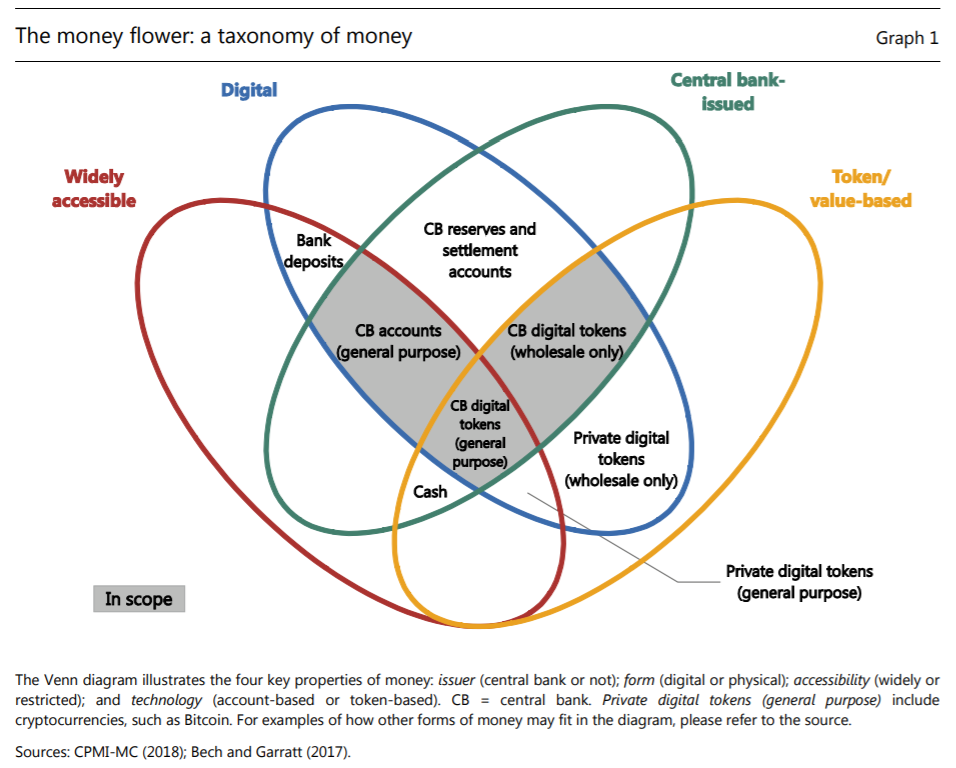

Financial infrastructure is an obtuse and arcane subject, and I’m always grateful to talk things through with a specialist like Robert Greene. Central Bank Digital Currencies (CBDCs) are a topic we’ve discussed at length before, but it seems recent events have really pushed them to the forefront. I do want to emphasize the views below are mine and not necessarily Robert’s – check out the video to learn more: https://www.youtube.com/watch?v=qjADjlJd90Q.

CBDCs have always been mystifying to me. Let’s be honest, almost no one has any idea what a CDBC really is. The various schemes that have been thrown around vary widely in both function and specificity. Libra has shifted significantly since it was announced and has given up on its original goal of a multi-asset backed global currency, opting for the much simpler design of digital versions of existing currencies. It reminds me a lot of my favorite definition of AI: “AI is what computers do in movies.” In that same vein, it feels like CBDCs are what blockchains do in the dreams of central bankers.

Again, my words, not Robert’s.

Still, let’s give CBDCs a fair shake and try to put together something that might work. In the video, we do some improv speculative fiction and poke at a model where CBDCs are basically a consumer bank account at the Fed. So it’s a dollar, there’s no interest, all your KYC and payment information also sits with the Fed, and everyone gets their now ubiquitous universal basic income payments via CBDC. And let’s assume every central bank in the world is using this.

Right away, there’s the obvious issue that banks (of the non-central variety) will be severely impacted. Traditionally, banks earn their keep by attracting deposits from customers by offering custody and interest, then getting a return on capital by lending it out. Now that everyone is keeping their money at the Fed, the deposits have stopped trickling down to normal banks. So let’s introduce another wrinkle: let’s assume this CBDC has an API that banks can plug into. A customer would see a prompt in their CBDC app that asks if they want to share their funds with Goldman Sachs Marcus, that the funds will be used to make loans, that they can expect interest of around X% per annum, and that there’s a certain element of risk. If they consent, their authorization is all that’s needed to whisk the funds away in the background from their account to Goldman Sachs, and the money starts getting put to work, along the rails of what the customer has authorized. This leaves space in the system for entities that are good at understanding and managing credit risk to live and thrive – something banks should be good at.

Immediately, the need for deposit insurance would be eliminated, because it’s impossible for the central bank to default on its own currency. The spectre of bank runs and bank defaults (including the risk of losses from highly levered derivative bets wiping out deposits from millions of retail customers) would be a thing of the past. Banks would only be able to bet as much capital as customers authorize them to use.

What about payments? What some people may not know is that payments already go through central banks. Domestically this is through some gross settlement system operated by the central bank (in the US it’s ACH), and internationally it’s through a network like SWIFT, which relies on central banks settling with each other (Faisal Khan has a great breakdown). A lot of the time, cost is padded on by non-central bank intermediaries in the form of extra fees, unfavorable exchange rates, and delayed settlement times (so your money can sit on their books for a while and earn interest). In a CBDC world, a customer sending money back home could go directly to an ECN forex broker, exchange their CBDCs at the market rate, get their foreign CBDCs immediately, and send them onwards to the recipient. The whole transaction would have no risk of default (since it is connected end-to-end via API to backed CBDC accounts), low risk of money laundering (since all payment information sits directly with the central bank, which presumably would collaborate with the relevant government agencies), and is much faster and cheaper for the customer. Meanwhile, payments companies like Square could still make money by offering a streamlined interface and value-added services to merchants, on top of nearly free and instantaneous CBDC domestic transfers.

There’s also a huge hidden benefit under the hood. Anyone who’s worked with bank IT systems lives in fear of the fact that the world’s wealth is ultimately reliant on creaking 90s mainframes running COBOL. For a bank to replace their core systems is like going through open heart surgery, and so they deal with the problem like anyone else: by avoiding it as long as possible. A shift to CBDCs would take this pressure off banks and remove risks of catastrophic IT failure from everyone else by making these systems obsolete, while unlocking the potential for new forms of innovation.

The end result is the decoupling of financial services: in a reversal of the trend over the last decade, where we saw a massive consolidation in financial services and the growth of a few full-service superbanks, CBDCs can enable lean market participants to provide services in only the areas they are competent in, without having to put up with the overhead of maintaining banking infrastructure. So long as regulation remains rigorous, this could mean much more transparency and competition for customers, and ultimately better service and lower fees.

To summarize, even in a simple scheme like this, CBDCs eliminate the risk of bank defaults, radically improve price transparency and settlement times for money transfers, and shift the foundations of the financial system onto a digitized, high-load backbone that’s more fit for the 21st century. The key for central banks to realize these benefits is to offer central bank accounts to everyone. The technology doesn’t actually matter. To me, focusing on how CBDC’s would work from a technological standpoint is missing the monetary system for the money.

To me, the real debate shouldn’t be about CBDCs, it should be about the role central banks will play in our lives in the future. We’re seeing a radical experiment play out where the impact of central banks (already greatly increased since the Great Financial Crisis) is again rising dramatically. Is this really what we want? If it is, then shifting to CBDCs is almost a given.

This leaves us with one last question: where does crypto fit in? The fact is, crypto already works like a CBDC. Anyone can get an account at the Bitcoin Fed (ie. download a Bitcoin wallet), all your payment information sits on the blockchain, there’s no interest, and service providers compete to utilize your Bitcoin. So at minimum, crypto can serve as a free-market petri dish for central banks to reference. There’s one big difference though: where central bank monetary policy is currently looser than pants after a successful weight loss program, Bitcoin’s monetary policy notoriously tightens over time. Only time will tell if that crucial difference is a competitive advantage or a death knell.